This moment — the last 10 seconds of the purchase journey — is now the biggest battleground in Indian ecommerce.

Checkout in India is in its fastest transition phase since 2016.

Two forces are shaping it:

- Behavioural psychology shifts (risk perception, instant gratification, effort threshold, trust anchors)

- Data-layer innovations (UPI deep linking, wallet survival mechanics, tokenisation, credit on UPI, new payment routing logic)

Brands that understand both don’t just reduce drop-offs —

They increase conversions by 12–27% simply by aligning with how Indians actually behave at checkout.

Not by adding discounts.

Not by redesigning the whole site.

But by engineering the checkout experience around India-specific psychology.

Let’s dive and decode The Future of Checkout in India: UPI, Wallets, and Beyond

The Psychology Behind Checkout Choices in India

1. UPI = Instant Control + Zero Cognitive Load

UPI works because it solves two psychological frictions at once:

- No card details (zero effort)

- Instant confirmation (zero uncertainty)

Why Indians gravitate toward UPI even when other methods exist

- Anything that requires typing → high friction

- Anything that delays success → high anxiety

- Anything involving banks → low trust

- Anything that gives instant push notification → high comfort

Result:

UPI now dominates because it aligns with lazy, risk-averse, decision-fatigued behaviour.

Category Patterns

- Beauty/Skin/Hair → Higher UPI success (impulse + low ticket value)

- Electronics → Mixed (UPI + Credit Card for EMI)

- Grocery → UPI almost always top performer

2. Wallets Work Only When There Is a Strong Habit Loop

Why wallets still survive despite UPI dominance

Wallet behaviour is built on:

- Stored value (people feel obligated to use it)

- Cashback memory (“I got rewarded before, so I trust this”)

- Single-tap checkout (speed bias)

When wallets outperform UPI

- Flash sales

- High-frequency categories

- Younger demographic (18–24)

- Tier 1 metro customers

But…

Without an existing habit, wallets rarely pull new users.

3. Cards Are No Longer “Default” — They Are Now “Utility-Driven”

What keeps card payments alive

- EMI needs

- Rewards ecosystem

- High-ticket trust perception

- Business purchases

Behavioural pattern

Cards now appear mostly when:

- The purchase is planned, not impulse

- The order value is ₹2,500+

- There is a cashback or points nudge

- Customer wants control over credit cycles

4. COD = Emotional Safety Net (Not a Payment Mode)

COD isn’t about “cash.”

It’s about:

- Fear of failed delivery

- Fear of fraud

- Fear of committing before receiving

COD psychology is strongest in

- New customers

- Tier 2/3 cities

- High-RTO segments (fashion + accessories)

- Low trust categories (health supplements, gadgets)

Even if COD declines, this fear-driven behaviour will remain unless trust levers replace it.

5. Checkout Abandonment Triggers Are Psychological, Not Technical

The moment someone drops off at checkout, it’s usually because:

- “This will take too long”

- “This looks suspicious”

- “Why do they need so many details?”

- “Will the payment fail?”

- “Do I trust this brand enough?”

Top friction points in Indian D2C checkout

- Mandatory login

- Long address forms

- Payment method not loading instantly

- Limited UPI options

- Gateway failure loops

- No retry options

- Lack of “instant guarantee” messaging

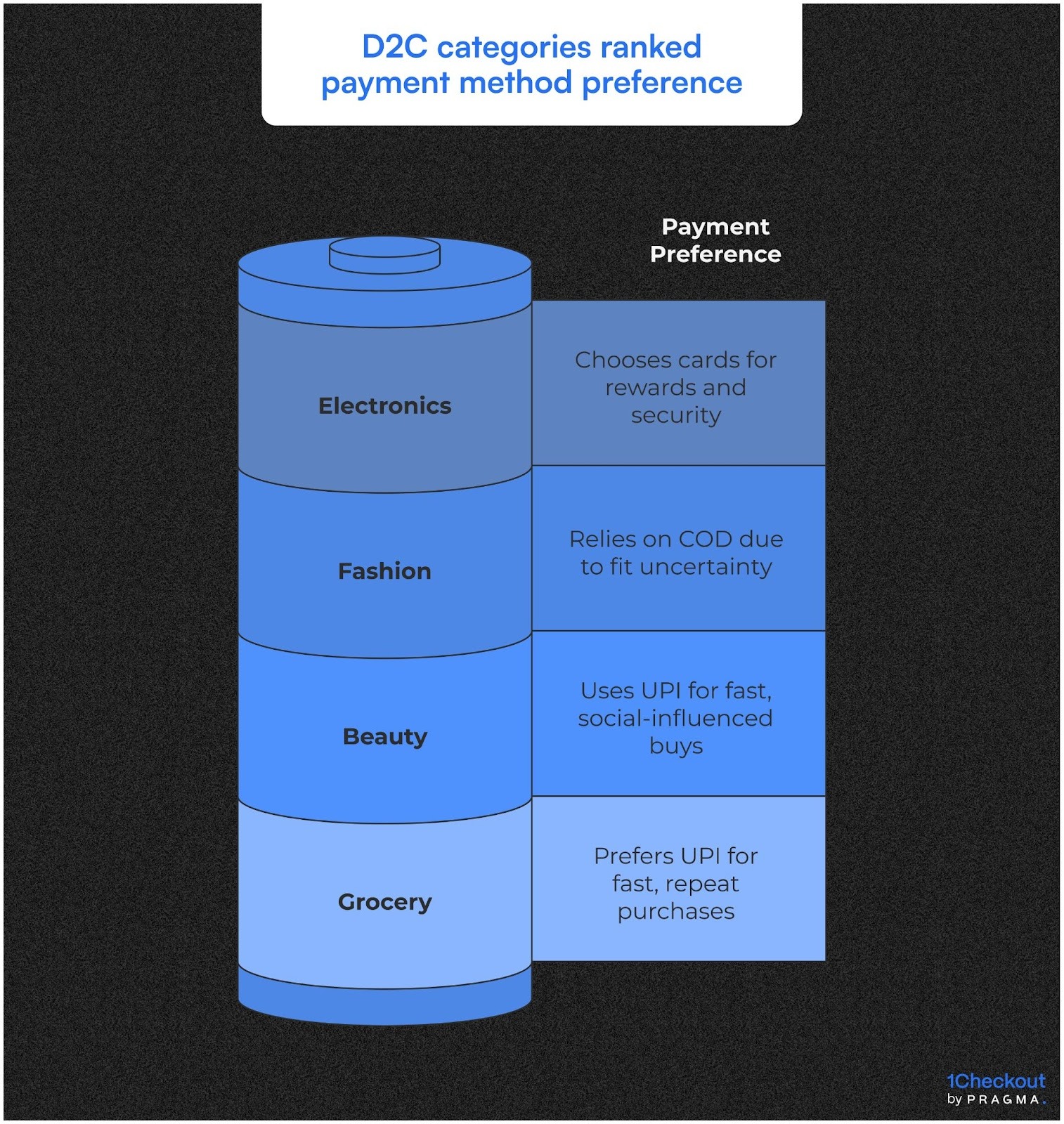

Category-Specific Checkout Behaviour in India

1. Beauty, Skin & Personal Care

Beauty and skin shoppers move fast because most purchases are impulse-led and influenced by social feeds.

The audience skews young, so UPI performs exceptionally well — they want fast, clean checkouts with zero typing.

Trust levers like “priority dispatch,” real-time tracking, and easy returns play a surprisingly big role because the category is flooded with new-age brands. If the checkout feels slow or asks for too many details, the user abandons instantly.

2. Fashion

Fashion has the highest COD dependence among all D2C categories in India. Shoppers often feel uncertainty around fit, fabric quality, and returns — so COD becomes their emotional safety net.

RTO rates spike here because browsing is casual and decisions change after delivery attempts.

Wallets see above-average action due to the younger demographic, but prepaid conversions struggle unless brands offer trust boosters like fit guarantees, flexible returns, or exchange-first options. Checkout clarity shapes confidence in this category.

3. Electronics

Electronics shoppers behave very differently: the category is high-ticket, research-heavy, and trust-sensitive. Buyers prefer cards because rewards, EMI options, and credit cycles align with the nature of the purchase.

UPI adoption is growing, but only where brand trust is already established; unknown brands see more drop-offs due to fear of post-payment disputes.

A clean, minimal checkout with strong reassurance elements — warranty badges, GST invoices, service guarantees — lifts prepaid conversions significantly.

4. Grocery & Daily Essentials

Grocery shoppers care about speed, habit, and reliability. This is one of the rare categories where the payment decision is almost subconscious — users go straight to UPI because it’s the fastest and because grocery purchases repeat weekly.

Wallets still perform well due to past cashback memories and a strong routine loop. COD is minimal because urgency outweighs caution.

The checkout must load instantly; even a 2–3 second delay drastically reduces conversion in this ultra-fast decision category.

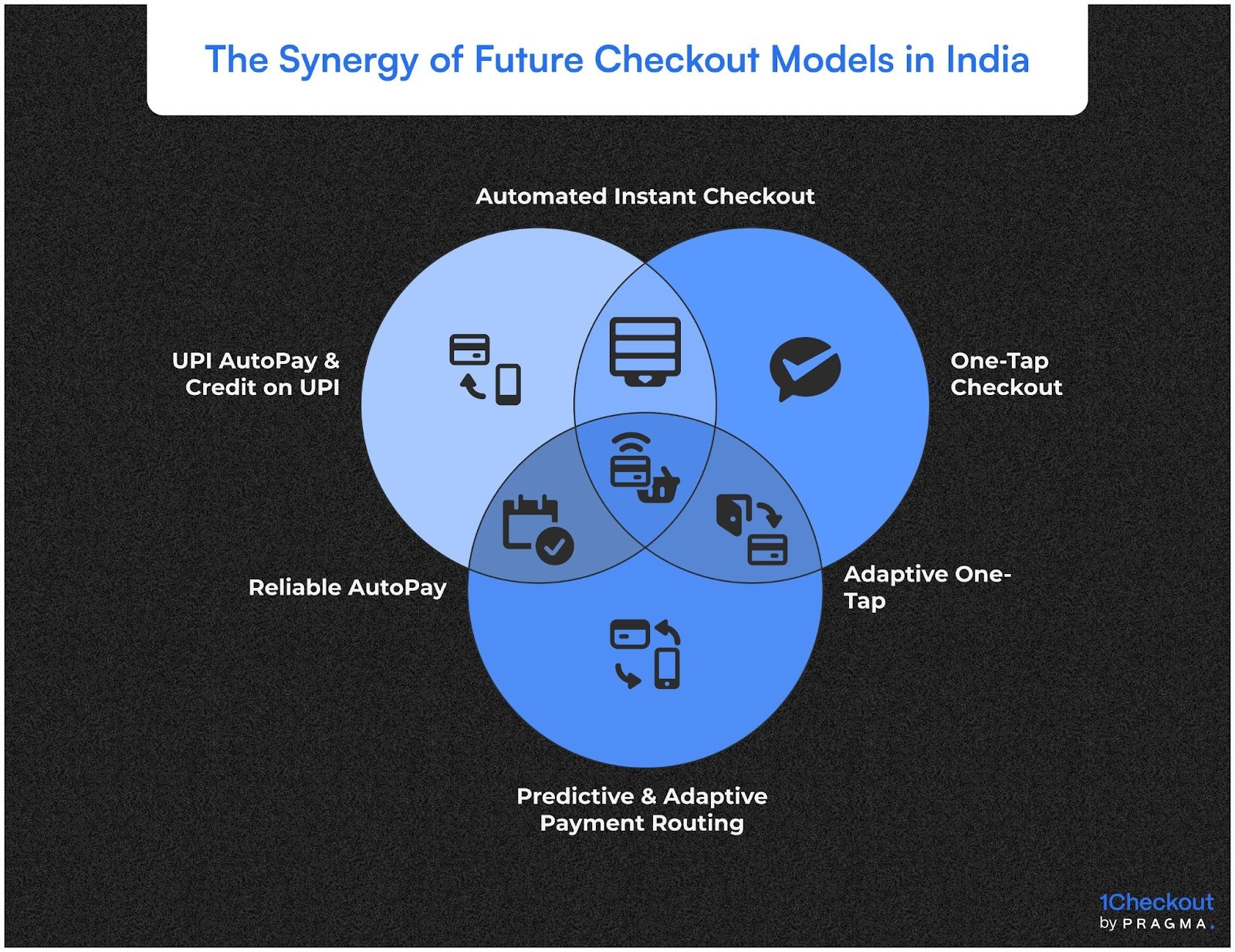

The Shift Toward Future Checkout Models in India

1. UPI AutoPay & Credit on UPI

UPI AutoPay is quietly becoming the backbone of frictionless repeat purchases. Users no longer want to re-authorise the same transaction every month, especially in categories like wellness, grooming refills, pet care, and home essentials.

AutoPay removes cognitive effort entirely — the user simply continues their routine, and the payment happens in the background.

Credit on UPI is reshaping higher-ticket shopping behaviour. Many buyers who avoided large UPI payments now prefer it because it merges instant approval with the familiarity of UPI flow.

This reduces the brand’s reliance on EMI placements or card tokenisation pop-ups that slow the checkout down. As credit scoring strengthens, mid-ticket segments like fashion, gadgets, and smart home devices will experience a meaningful uplift in prepaid conversions.

2. One-Tap Checkout via Magic Links, WhatsApp, or Native Apps

One-tap checkout compresses the entire purchase flow into a single confirmation action. Instead of typing, verifying, and selecting options, the user receives a pre-filled, pre-verified checkout link that carries their historical preferences.

For returning customers with strong purchase intent, this becomes the fastest path from decision to payment.

WhatsApp-led one-tap flows push conversion even higher because the channel feels familiar and frictionless. The user simply taps a verified link, selects their saved method, and completes the payment instantly.

Native shop apps take this further by eliminating passwords, supporting biometrics, and predicting the default payment method — creating a checkout that feels almost invisible.

This is especially valuable for impulse-prone categories where speed decides whether the sale happens at all.

3. Predictive & Adaptive Payment Routing

Adaptive routing marks the shift from static payment attempts to intelligent success-driven flows. Instead of sending every transaction through a fixed path, the system evaluates bank uptime, payment load, issuer behaviour, and risk flags in real time.

The gateway then pushes the transaction through the route with the highest probability of success.

This approach benefits India’s fragmented banking reliability, where issuer downtime fluctuates hour by hour.

A smart router detects these patterns, bypasses unstable issuers, and reduces payment failures that frustrate users. The result is a 3–7% improvement in payment success rate, purely through smarter routing logic — no UX changes required.

Over time, adaptive routing will also learn individual user patterns. It will recognise which card, VPA, or wallet a shopper reliably uses and prioritise that path, eliminating unnecessary friction and strengthening their checkout completion habit.

Quick Wins from Observing Future Checkout Options

Short operational improvements that immediately strengthen checkout performance.

Week 1 — Simplify Payment Visibility

Most brands underestimate how much choice overload slows Indian buyers.

Reducing payment clutter helps shoppers reach their preferred method faster, especially when UPI already contributes over 78% of digital payments in India (NPCI, 2024).

Show UPI first, fold card options, and hide lesser-used wallets unless specifically tapped open.

Week 2 — Repair Broken Micro-Interactions

Micro-interactions guide the moment a user decides to complete a purchase.

Fix delayed bank redirects, unresponsive pay buttons, unclear error labels, and incomplete loaders.

These tiny fixes prevent high-intent customers from dropping off due to avoidable confusion.

Week 3 — Implement Smart Retries for Failed Payments

Smart retries reduce drop-offs by recovering failed transactions without pestering users.

Customers prefer a retry prompt that feels contextual, not pushy, especially when failures happen due to issuer downtime or UPI handle latency.

Brands that implement conditional retries often recover 6–9% of failed payments within 30 minutes.

Week 4 — Deploy Behaviour-Based Payment Nudges

Nudges work when they appear only at moments of hesitation.

Reminding users that their favourite method “works fastest” or that their “saved UPI ID is available” reduces decision fatigue.

Behavioural alignment increases prepaid conversions without feeling intrusive.

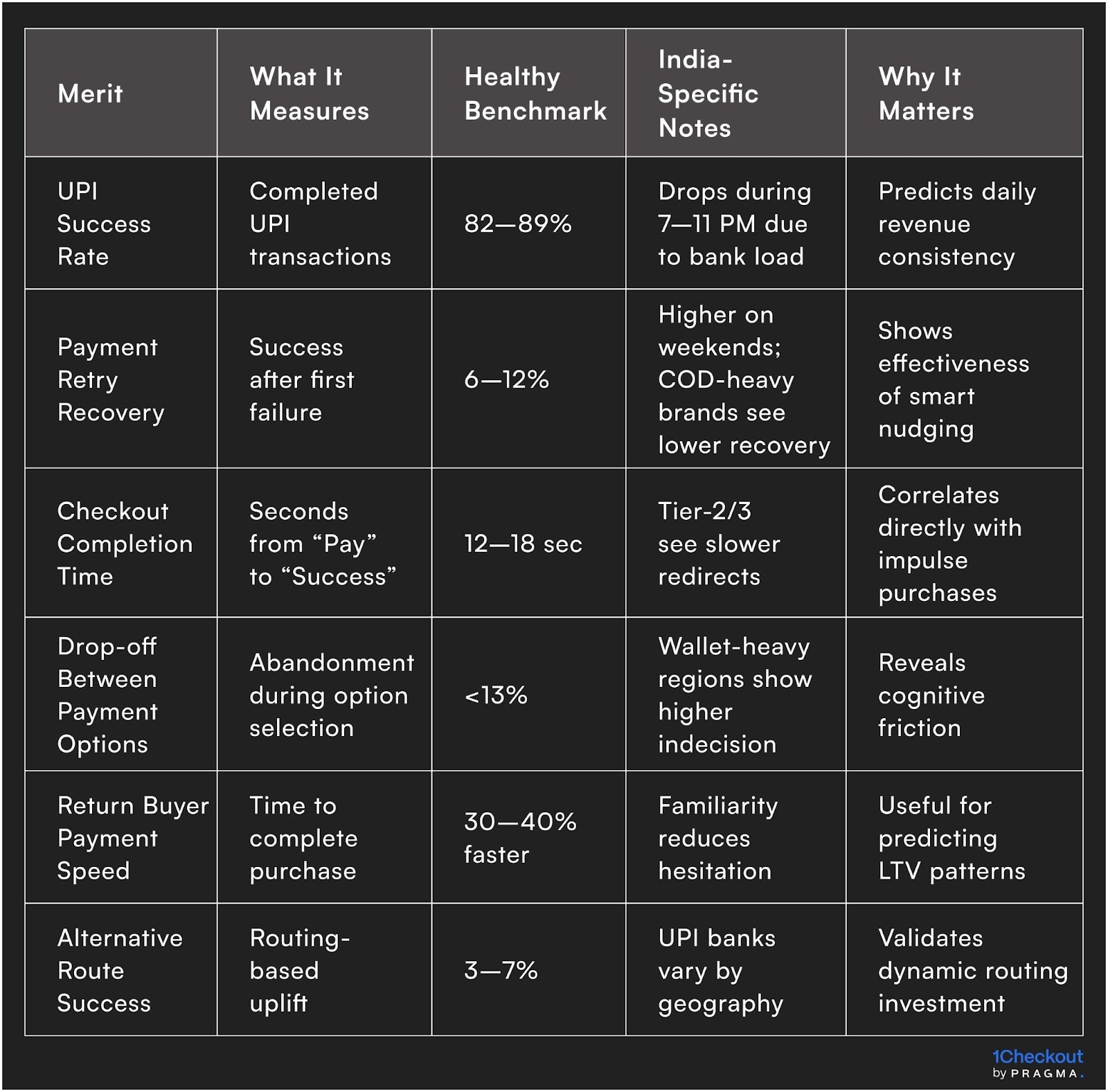

Which Metrics Actually Matter for Checkout Performance?

Data points that reveal where your friction truly lies.

To Wrap It Up

The future of Indian checkout flows will rely on simplicity, behavioural alignment, and the intelligent use of payment data. The brands that understand how buyers decide, hesitate, and repeat familiar actions will shape the next phase of prepaid adoption across categories.

Start by fixing micro-frictions in your existing flow before adding new payment layers.

Long-term advantage comes from capturing payment signals, adapting routing logic, and shaping familiar patterns that shorten checkout time for every returning buyer.

For D2C brands seeking to streamline payment reliability, Pragma’s Checkout Intelligence provides adaptive routing, behavioural nudges, and real-time monitoring that consistently uplifts payment success rates across Indian regions.

.gif)

FAQs (Frequently Asked Questions on The Future of Checkout in India: UPI, Wallets, and Beyond)

1. Why do UPI failures spike at certain hours?

UPI failures rise during high-load times when specific issuers throttle transaction processing. This pattern is common in metros between 7–11 PM and causes sudden dips in success rates.

2. Does too many payment options actually reduce conversions?

Yes. When users face too many choices, they hesitate longer. A simplified, predictable payment layout usually converts better.

3. How do COD-heavy brands shift customers to prepaid?

Brands typically use convenience-led nudges like faster dispatch or instant confirmation. The shift is gradual because behavioural trust takes time to build.

4. Is UPI safer than card payments?

UPI is considered safer for most users due to real-time authorisation inside the banking app. Fraud tends to occur outside the payment flow, not within it.

5. Should payment retries be hidden or openly shown?

Retries work best when transparent and contextual. Users appreciate clarity when a failure occurs due to bank downtime or routing issues.